Our organization is at a critical turning point because of failing the SOC 2 audit. We believed that we were ready, that policies were registered, security tools were properly placed, and that we had proper evidence. But with the commencement of the audit, the loopholes in documentation, surveillance, ownership, and controls soon became evident. Formal exceptions came out of what we believed was going on with the stuff that should be disorganized. These are the seven crucial mistakes that will eventually cost us our SOC 2 audit victory.

7 common Mistakes of SOC 2 audit that you must avoid

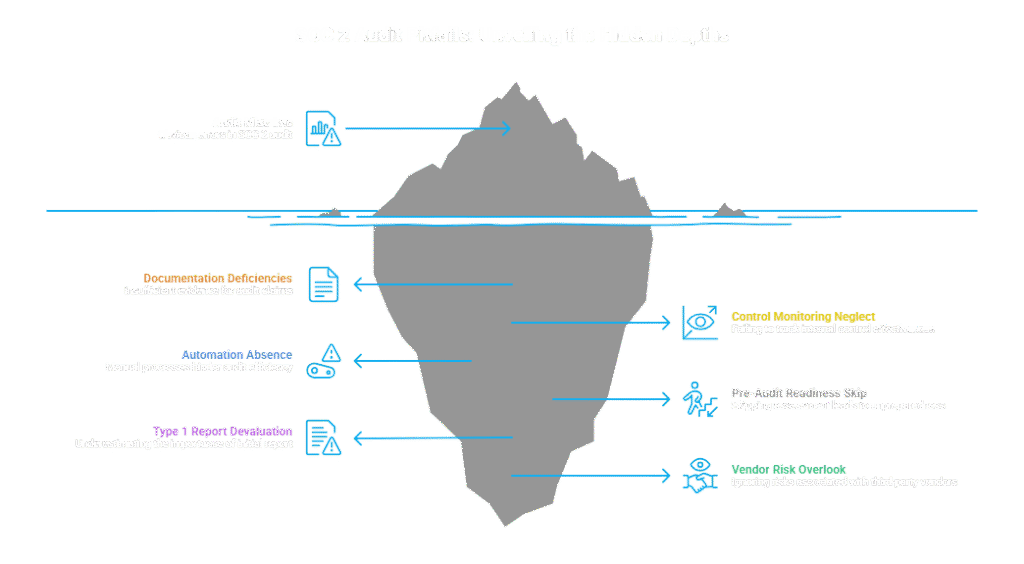

SOC 2 audit requires preparation, discipline, and cross-functional accountability. We learned a bitter lesson that even minor details can lead to significant insights. These are seven pitfalls that we faced.

1. Mistaking SOC 2 Audits as Security-Only Assessments

We falsely assumed that the SOC 2 audit was a cybersecurity audit only. Though security is among the Trust Services Criteria, SOC 2 extends much further than firewalls, encryption, and vulnerability scans. We have prepared with IT security controls only, and this has left loopholes.

SOC 2 focuses on governance composition, risk control procedures, vendor management, access control, change control, incident control, and even the HR procedures, including onboarding and termination of employees. Our leadership, operations, compliance, and engineering teams are not aligned, and auditors have swiftly found control weaknesses beyond the security department.

The result of our misconception has brought about incomplete documentation, a lack of ownership of controls, and a lack of coherence in enforcing policies. Consequently, we scrambled during the audit to find missing evidence in the departments.

A SOC 2 audit is not only a technical test but a cross-functional operational audit. We have also taken it as security-only, which has broken the audit friction and compromised the trustworthiness of our general compliance posture.

2. Lack of evidence-based SOC 2 audit documentation

When the external auditor asked us to provide access logs, we showed them our final Excel file without an explicit explanation of the evidence and well-organized SOC 2 documentation. The SOC 2 audit is not only about documentation; it is the basis of the attestation. The auditors have to ensure that the controls are not only designed appropriately, but they should also be working effectively in the long term. Random screenshots, mismatched file names, missing time and date, or unconfirmed export have undermined our evidence.

Since SOC 2 is an attestation engagement that is carried out in line with AICPA standards, auditors are cautious to abide by those rules. Auditors increased testing, demanded more samples, and undertook further validation as our documentation appeared to be disorganized or incomplete. This has escalated audit time, postponed the provision of reports, and caused cost escalation. What is more important is that it caused uncertainty regarding the level of control maturity, and governance practices in your organization; therefore, take note.

Operational discipline is indicated by strong, centralized, and clearly mapped evidence. Conversely, poor documentation is an indicator of risk, and the absence of evidence-based documentation of our audit is therefore an expensive but preventable error.

3. Neglecting ongoing internal control monitoring

Similar to most organizations, we have also instituted controls at the start of the audit period, but we do not continue to audit, test, and ensure the validity of the controls over the passage of time. During a SOC 2 Type II audit, auditors do not simply evaluate the design of controls, but also determine how they worked consistently during the period covered by the audit.

Without regular monitoring, gaps go unnoticed without frequent internal reviews, such as missed access reviews, unfinished log monitoring, delayed patch updates, or unassessed policy exceptions. Once these lapses are identified in the audit, the remediation is reactive and stressful, and may need extra testing or increased scope.

Monitoring demonstrates that conformity is ingrained in day-to-day activities and not an end-of-day practice. Companies that set quarterly reviews, automatic notification, sign-offs by management, and written monitoring have a substantially lower audit risk.

Ongoing auditing enhances responsibility and fosters assurance in the auditors, and its absence maximizes discovery, expenditure, and publicity.

4. Lack of automation in the SOC 2 audit process

The use of manual spreadsheets, email trails, and screenshots to glean and track audit evidence has become a leading issue with SOC 2 audit failure. Although this can be effective in the short term, it has caused inefficiency, version control issues, and increased risk of human error. The use of manual operations renders it hard to show concurrent control operations, particularly when undertaking a SOC 2 Type II audit over a period of multiple months.

In the absence of automation, such activities as access checks, log checks, ticket tracking, and evidence collection need manual and repetitive efforts. This does not just waste the precious team time, but also raises the chances of missed reviews, incomplete documentation, or obsolete records.

We therefore suggest automation tools to assist in the centralization of evidence, establish audit trails, plan recurring control activities, and keep an up-to-date status of compliance. They make the company less dependent on people and make it more consistent in reporting periods.

Consistency and reliability are important in a SOC 2 audit. Firms that are not automated do not have scalability, accuracy, and audit readiness, which causes delays, escalating costs, and unwarranted audit friction.

5. Skipping a pre-audit readiness assessment

There is a risk of causing unwarranted risks and procrastination in our compliance pathway just by skipping a pre-audit readiness assessment. When we launched ourselves directly into a formal audit, we did not carefully review our current controls and usually failed to notice flaws in documentation, policy fit, and evidence gathering. This led to unwanted results, which meant escalated expenses, protracted schedules, and tainted internal resources.

Because of the absence of the SOC 2 preparedness, we were not aware of whether our systems, processes, and security controls are up to the necessary standards. Our evidence was partial and has impacted the confidence of the auditor in our control environment. It has also restricted our desire to take a proactive action to identify our weaknesses prior to them becoming official audit observations.

A readiness test will help us know about gaps at early stages, safeguard our reputation, and enhance our long-term compliance stance.

6. Devaluing the importance of the Type 1 report

We have taken Type I as a pre-guide and emphasized attaining a Type II report. Type I audit, however, is critical in its foundation. It determines if the controls are designed correctly at a given time, and the organization tests that their compliance framework is in place in the right way before they enter into a long monitoring phase.

Underperformance of Type I has led to improperly designed controls being put to test over months of a Type II audit, and this heightens the chances of exceptions and expensive remediation. Type I holds a preparation check.

Moreover, we have also seen that most of the customers will believe a Type I report is prioritized by early-stage companies as a sign of compliance determination, rather than as an indication of the development and maturity of governance for already established companies.

The perception that Type I is not material may slow compliance success, predispose heightened audit risk in the long term, and compromise your overall SOC 2 strategy.

- Overlooking vendor risk management during the audit

The biggest error we have made is the fact that we have assumed that when we choose a third-party provider, the responsibility is transferred to the vendor. The fact is that SOC 2 obligates the organizations to ensure that they have control over any third party that stores, processes, or transmits sensitive data on their behalf.

Auditors demand clear records and the vendors should be assessed prior to the onboarding process and supervised during the relationship. These are keeping a vendor inventory, due diligence reviews, reviewing vendor SOC reports, contract term tracking, and recording risk identification responses. The absence of this evidence can make auditors doubt the appropriateness of governance of external dependencies.

Assessing vendor controls is necessary to avoid introducing any hidden security, availability, or confidentiality risk into the environment. Although you may have internal systems that are well controlled, vendor-level weakness may undermine compliance.

Effective vendor risk management is accountable beyond the organizational boundaries. Its neglect is an indicator of an unfinished risk management process, and may result in audit discrepancies, further investigation, and reputational damage such as ours.

Conclusion

Our SOC 2 audit failed because of multiple preventable errors. Our underrated preparation, documentation, discipline, inter-functional coordination, and monitoring have led to the situation. As per our experience, SOC 2 is not merely a compliance step, but an operational maturity test. These errors may be avoided through good planning, automation, monitoring, and preparedness testing. Working with an expert compliance advisor like Matayo can help you to simplify the process, strengthen security controls, and complete the SOC 2 audit with confidence and clarity.