Cybercriminals are targeting startups and small businesses to extract confidential data, and the rate is currently at 70 percent. Regardless of this frightening trend, most business owners do not realize that compliance with PCI is not only a concern for the big companies but also for entrepreneurs and small and medium enterprises. The PCI DSS compliance will give a roadmap to protection, and the contemporary automation systems can reduce the manual load of compliance by 90%. Limited resources, evolving technology bases, and lack of ownership are common pitfalls that even startups can avoid when a basic checklist is combined with automation and a committed PCI lead can bring compliance out of a frantic scramble and transform it into a scalable, standard practice.

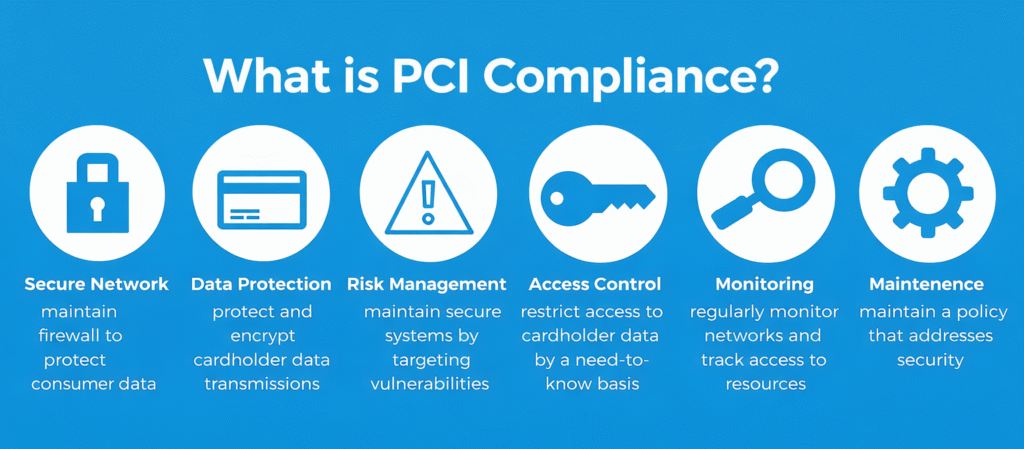

What is PCI Compliance?

Payment Card Industry Data Security Standards (PCI DSS) are used in any company that maintains, handles, or transfers credit card information. It makes it simpler to embrace the overall application of standard data security measures. Web companies should be in line with the requirements of PCI DSS, which involve the requirement of hosting the data in a PCI-compliant host. The major credit card companies, including Visa, Mastercard, Discover, and American Express, adhered to PCI DSS compliance. The primary objective of PCI compliance is to minimize the attack opportunities. This includes the utilization of a secure Card Data Environment (CDE), and this is irrespective of whether you are utilizing your in-house setup or a third-party safe payment option. This is particularly crucial in the case of e-commerce websites, where the transfer of payment card information is all that is involved via the internet.

Significance of PCI DSS Compliance to Start-ups and SMEs

In the new digital-first economy, online transactions, subscription billing, and digital payment gateways are becoming more essential to startups and SMEs. It does not matter whether you are creating a fintech application, SaaS, eCommerce site, or a health-tech solution; cardholder data is something that must not be compromised.

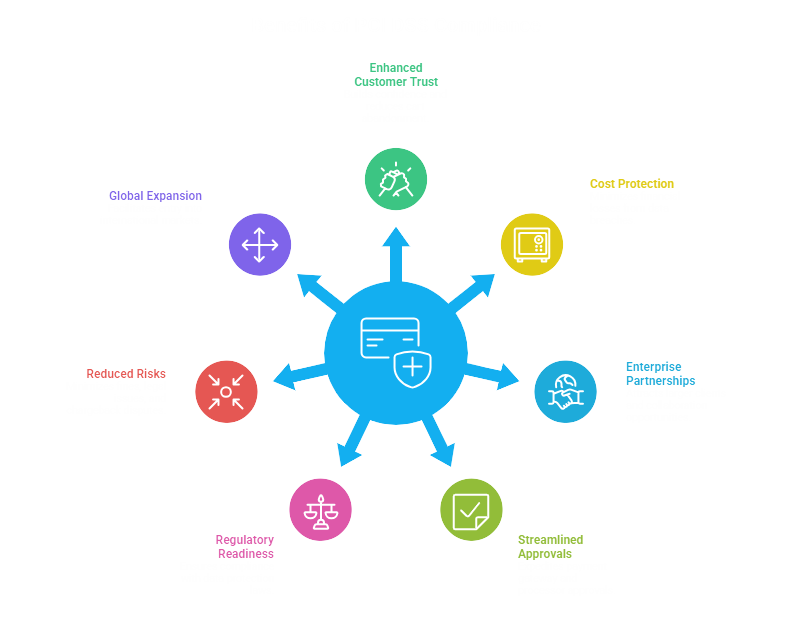

Builds Instant Trust with Customers

The customers are more privacy-conscious than others. Information breaches and fraud have made people more cautious about protecting private information, especially when they key in their sensitive data. So, if your startup has been found to be PCI DSS compliant, it shows that you have been following security controls like encryption, network monitoring, secure access management, and vulnerability testing.

Trust has a direct influence on purchasing. Showing safe payment handling behavior lowers the rate of cart abandonment and guarantees customers that their card information is secure. To the SMEs that are competing against established brands, compliance is a boost to credibility and a level playing field.

Protects You from Costly Data Breaches

Small and mid-sized enterprises are disproportionate targets of cyberattacks due to their tendency to be less secure than larger enterprises. The requirements of PCI DSS include a firewall, strong password optimization, proper system settings, encryption, and frequent testing. Such controls would help to minimize the chances of breaches.

One instance of data breach is enough to cost startups lakhs, or even crores, in conducting investigations, litigation, refunding customers, and reputational damages. Recovery time can halt growth and investor confidence, in addition to financial loss. Compliance assists in creating a strong security infrastructure framework that can avoid such disastrous failures.

Attracts Enterprise Clients and Partnerships

Enterprises and international companies have high security demands on vendors and partners. B2B and fintech integrations and payment partnerships are made conditional upon the PCI DSS compliance.

In case your startup targets banks, marketplaces, SaaS aggregators, or other global customers, being PCI compliant shows the maturity of operations. It will also assure them that you have payment systems that will not put them at third-party risk, which will make them prefer to collaborate with you over others.

{kind=link}

Simplifies Payment Gateway and Processor Approvals

Before accepting businesses, payment processors and acquiring banks evaluate risk. By showing PCI DSS compliance, approvals are expedited and could lead to the simplification of integrating with gateways.

Businesses that are not compliant usually get subjected to increased scrutiny, monitoring, and other fees. Compliance eases friction and makes audits easier, enabling continuous processing of transactions, which are essential in digital sectors.

Ensures Regulatory Readiness

Data protection laws have strengthened their efficiency level. PCI DSS is a complementary model like the General Data Protection Regulation (GDPR), and the Digital Personal Data Protection Act 2023 (DPDP Act). Though PCI DSS is focused on the cardholder data, the controls are rather similar to the general data protection controls, including access control, data minimization, encryption, and monitoring. Compliance ensures that your overall business governance posture is enhanced and that your business is ready to go through regulatory audits.

Reduces Fines, Legal Risks & Chargeback Disputes

Failure to comply may result in hefty fines by payment, particularly following a breach. Also, lawsuits, card replacement expenses, and higher chargeback ratios can be experienced by the startups.

Businesses reduce fraud and disputes on transactions by putting into effect the controls of PCI DSS. Fewer chargebacks help you to save your merchant account image and avoid the increased processing cost or termination of your account.

Future-Proofs You for Global Expansion

If your start-up intends to expand into foreign markets, PCI DSS compliance is a must. It is widely known and may be required when processing cross-border payments.

Investors, international business partners, and customers are always inclined towards the favour of adequate cybersecurity governance. Being PCI compliant shows long-term vision, ability to manage risks, and willingness to compete globally.

PCI Compliance Roadmap Startup and SME

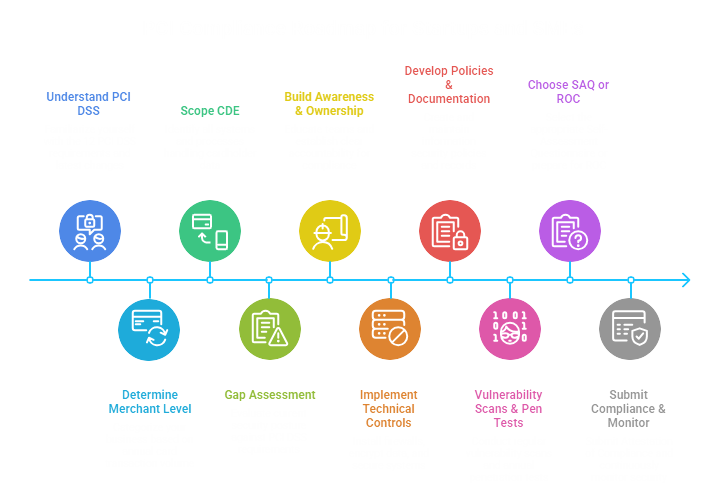

Compliance has a structured approach that is guided by industry direction on best practices provided by the top payment brands, as well as the cybersecurity bodies. The following is a realistic 10-step roadmap that can be used in growing businesses.

Step 1: Understand What PCI DSS Requires

The 12 requirements that the PCI DSS is based on are network security, encryption, access control, monitoring, and testing. Start by understanding the changes in the PCI DSS, such as installation of firewalls, securing the stored cardholder data, encryption of transmission, limited access, and regular monitoring of the systems. The awareness of these background needs helps you in judging the effort, tools, and skills needed.

Step 2: Determine Your Merchant Level

The PCI DSS compliance requirement depends on the size of your business, according to annual card transactions. Large payment systems such as Visa Inc. and Mastercard group merchants into four categories depending on the volumes of transactions and risk assumption.

Level 1 encompasses a business that does more than 6 million transactions annually. These are merchants who are subjected to the most rigorous requirements, such as an annual on-site audit by a Qualified Security Assessor (QSA) and a more exact Report on Compliance (ROC).

Level 2-4 is applicable to merchants who produce lower transaction volumes. Level 3 or 4 startups and SMEs may also become compliant by completing a Self-Assessment Questionnaire (SAQ) and performing quarterly vulnerability scans, which simplifies and further lowers the cost of the aforementioned process even more.

Step 3: Scope Your Cardholder Data Environment (CDE)

Identify where the data of cardholders is kept, after it has been stored, processed, or transmitted. Your Cardholder Data (CDE) encompasses payment applications, servers, networks, and even third-party integrations.

Limiting scope by outsourcing payment processing can significantly reduce compliance complexity and costs. Proper scoping will avoid unnecessary security investments and will also cover everything.

Step 4: Conduct a Gap Assessment

A gap assessment is used to compare your current security posture and PCI DSS requirements. Check firewall policies, passwords, encryption policies, logs, and access control.

This step brings out the points of weakness and focuses on the remediation. Numerous startups also use the services of a Qualified Security Assessor (QSA).

Step 5: Build Internal Awareness & Ownership

IT is not the only responsibility of PCI compliance. Consult with an expert about PCI DSS to securely store customer data, payments, and infrastructure handling teams.

Proper accountability also helps maintain compliance with the policies, such as secure coding guidelines, limited access regulations, and incident-response procedures.

Step 6: Implement Technical Controls

According to your gap analysis, establish significant technical controls to comply with the Payment Card Industry Data Security Standard. Install firewalls and network segmentation to separate the Cardholder Data Environment (CDE). Secure the cardholder data by using a high level of encryption during rest as well as in transit. Use multi-factor authentication (MFA) to get into the system. Install the anti-malware systems on all terminals and servers. Lastly, ensure safe system administration by turning off default options and implementing security patches in time.

Step 7: Develop PCI Policies and Documentation

Documentation is critical. Prepare information security, access control, information retention, vendor management, and incident response documentation. Audit preparedness is ensured through maintaining records, change management documentation, and evidence of security testing.

Step 8: Perform Vulnerability Scans & Pen Tests

It has to undergo frequent testing. Retain Approved Scanning Vendors (ASV) by scanning vulnerabilities quarterly. Penetration testing is conducted on a yearly basis to ensure your security controls are robust. Weaknesses are detected prior to exploitation by attackers, and improve your total cybersecurity posture.

Step 9: Choose the Right SAQ or Prepare for ROC

The vast majority of the startups fill in the relevant Self-Assessment Questionnaire (SAQ), which is based on the model of payment integration (e.g., SAQ A in case of completely outsourced eCommerce).

Merchants with more than 30 employees might have to have a Report on Compliance (ROC), which is done by a QSA. The right validation method will make the reporting accurate and prevent penalties.

Step 10: Submit Compliance and Monitor Continuously

Send your compliance Attestation of Compliance (AOC) to your acquiring bank or payment processor. However, PCI DSS is not a project in itself, and it presupposes continuous monitoring, log periodic reviews, frequent tests, and policy amendments. Its ability to keep up with the requirements of the authorities, such as the PCI Security Standards Council, will enable it to be compliant in the long term.

Conclusion

PCI DSS compliance is a business enabler that helps build customer trust, initiate business relationships, and demonstrate to business partners that you are a serious security player. Compliance is a competitive edge in the case of startups and small businesses, whereby the wise selection of architectures, automated continuous monitoring, and the application of security in daily business operations. The most appropriate approach is that an emerging business should have the best practices of being audit-driven and having a constant watch on compliance. Seeking to make the PCI DSS compliance process simpler, start a partnership with Matayo to achieve quick certification, reduce risk, and scale security.